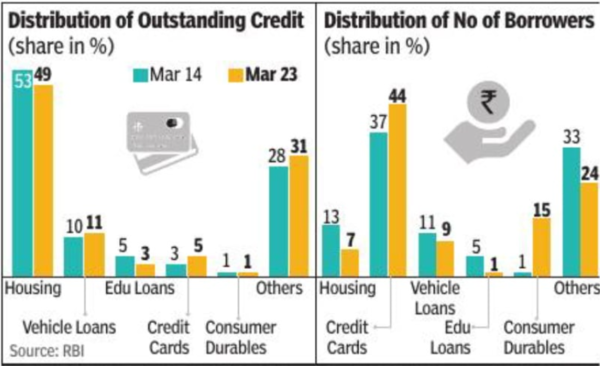

According to the study, over the past decade, there has been a big shift in the sectoral composition of bank credit due to growth in personal loans or retail credit in the overall credit portfolio. “As of June 2023, personal loans constituted the single largest category of bank credit, accounting for 49% of total borrower accounts, and 30% of the outstanding non-food credit,” it said. While the report did not specify the segments, it said that credit cards and vehicle loan portfolios did record a moderate but statistically significant rise in stress.

The study, which is authored by RBI staff, said that “pre-emptive macroprudential measures by the regulator augur well for financial stability”. The publication comes in the wake of RBI increasing risk weightage on unsecured loans.

The study said the emer gence of retail credit’s dominance in overall credit growth is by its long-term trends. “However, it needs to be ascertained whether the credit flow is towards appropriate borrowers without causing any risk to build up,” it said.

It said that while there are better-quality (more creditworthy) customers who get larger loans in most loan products, the reverse is true in the case of credit cards. “In the case of credit cards, per borrower credit outstanding is higher for the below prime borrowers, suggesting a higher flow of credit to relatively riskier borrowers,” the study said.

Most credit products recorded a significant rise in credit growth after Covid period as compared to before.